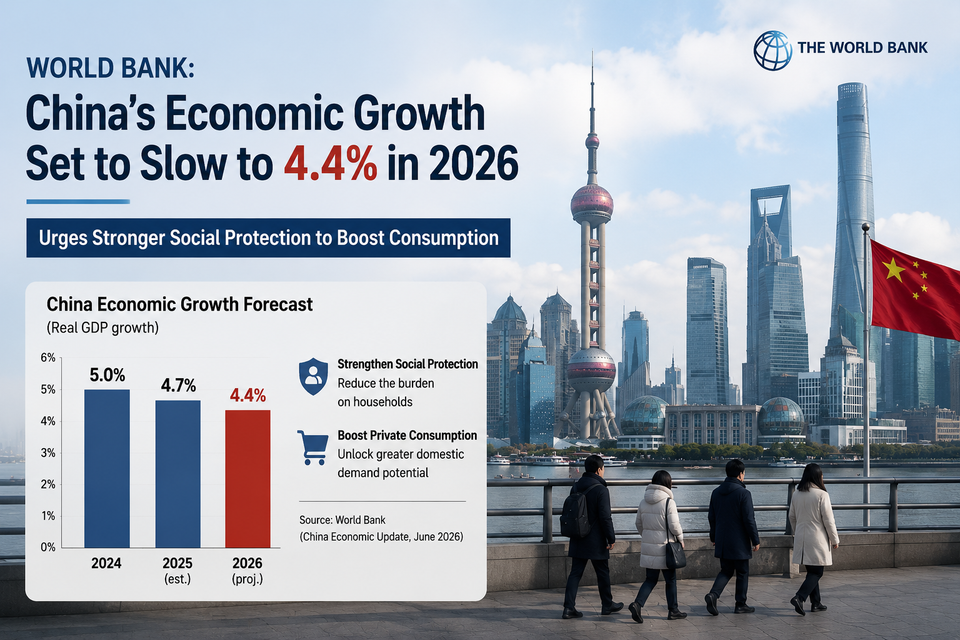

World Bank Sees China Growth Slowing to 4.4% in 2026

The World Bank says China’s growth may slow to 4.4% in 2026 and urges stronger social protection to support household consumption.

首次合成约需 20 秒,之后再访即点即听

China’s economy is expected to slow to 4.4% in 2026 from 5.0% in 2025, the World Bank said in its July China Economic Update, urging Beijing to shift more fiscal support toward social protection if it wants households to spend more.

The report, based on data available through June 30, said China’s economy began the year with some resilience. First-quarter GDP grew 5.0% from a year earlier, up from 4.5% in the previous quarter, helped by high-tech investment and strong exports.

Momentum weakened in the second quarter. Higher energy costs, external uncertainty and weak domestic demand weighed on activity. Inflation rose to 1.1% between March and May, though the World Bank described the energy-driven price pressure as likely temporary.

Under the bank’s baseline forecast, growth is set to slow further to 4.3% in 2027 and 4.2% in 2028. Consumption is expected to stay subdued, the property market adjustment is not over, private investment remains constrained by weaker corporate profits, and export growth is likely to ease as foreign demand cools.

Exports were still a major support in the first five months of the year. In dollar terms, they rose 15.5% from a year earlier, compared with 5.5% growth in 2025. High-tech manufacturing exports increased by almost 31%, boosted by global demand linked to the artificial intelligence investment cycle. Labor-intensive exports such as clothing, footwear and furniture remained weak.

Domestic demand did not recover at the same pace. Falling home prices, a soft labor market and slower income growth kept households cautious. Easier credit conditions have not translated into a clear pickup in borrowing by households or companies.

The World Bank placed much of the policy focus on how China spends public money. Capital spending still accounts for 43% of China’s fiscal budget, far above the OECD average of 13.5%. Health, education and social security together account for only 28%, compared with more than 60% in OECD economies.

Social spending rose 4.7% in the first five months, helped by higher childcare subsidies and support for disabled elderly people, but its share of GDP was broadly unchanged. The overall spending mix remains tilted toward investment.

China’s social protection spending is about 11% of GDP, roughly half the OECD average. Household savings exceed 30% of disposable income, more than twice the OECD average. Low retirement income, high out-of-pocket medical costs and unemployment risk are among the reasons households keep saving rather than spending.

The gaps are clear in pensions and health care. Migrant workers and informal-sector workers covered by the urban-rural resident pension system receive an average pension of 246 yuan a month. Formal urban employees in the contributory pension system receive a replacement rate of about 41%. Households still pay about 35% of medical costs out of pocket, while unemployment insurance covers less than half of the urban labor force and almost no migrant workers.

The World Bank estimated that doubling resident pensions could raise total household consumption by 2% to 4%. Raising resident medical insurance to the level of employee medical insurance could lift affected urban household consumption by 3.3 percentage points and rural household consumption by 5.6 percentage points. The report called for higher minimum benefits, broader coverage for flexible and informal workers, and access to services based on residence rather than household registration.

Real estate remains a downside risk. A deeper-than-expected property downturn would further hit household wealth and tighten financing for developers, weighing on consumption and property-related investment. Falling land sales are already squeezing local governments; land transfer revenue dropped 28.7% in the first five months.

Policy support and stronger AI-related investment are the main upside risks. Beijing could introduce a supplementary budget if growth pressure intensifies, while AI investment may run hotter than expected. Over the medium term, the World Bank said China’s shift toward consumption-led growth will depend on social security, fiscal and labor-market reforms.

Source note: This article is based on the World Bank’s July 2026 China Economic Update PDF. The report’s data cutoff was June 30, 2026.

You read this far. You're not here for noise.

SharpPost delivers one weekly deep dive on geopolitics, finance, and tech — decoded for readers who want signal. No ads, no filler.